Falling behind on mortgage payments can have long-lasting financial consequences, as delinquent payments can significantly damage a borrower’s credit score and remain on a credit report for up to seven years.

While some level of mortgage delinquency is expected, rising delinquency rates across a state can also signal broader economic strain. To determine where homeowners are struggling the most, WalletHub analyzed proprietary user data comparing mortgage delinquency rates from the fourth quarter of 2025 through the first quarter of 2026.

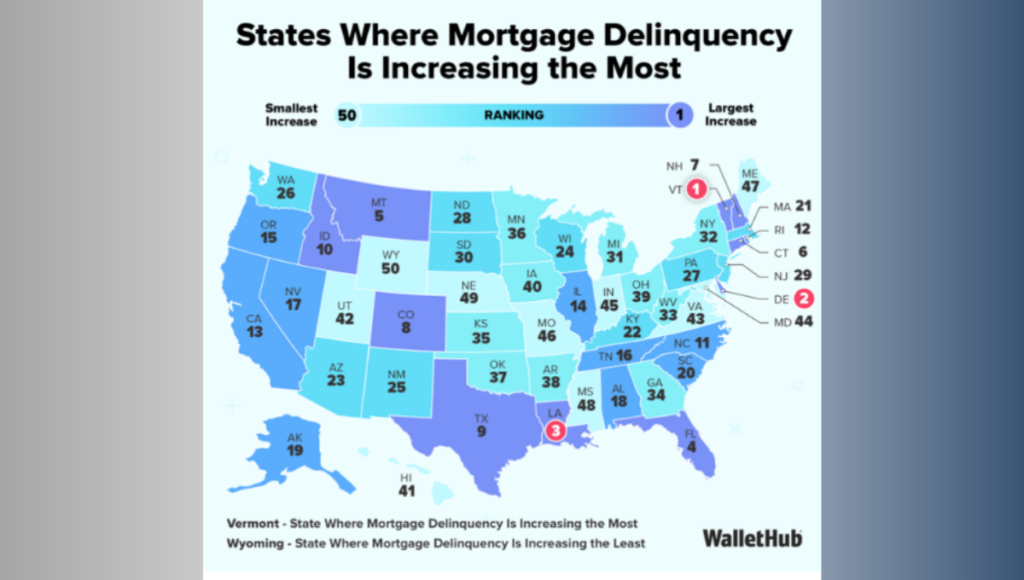

States Where Mortgage Delinquency Is Increasing the Most

| Overall Rank* | State | Share of Average No. Mortgage Loans Delinquent in Q1 2026 | Change in Average No. Mortgage Loans Delinquent (Q1 2026 vs. Q4 2025) |

|---|---|---|---|

| 1 | Vermont | 5.81% | 12.32% |

| 2 | Delaware | 8.35% | 6.92% |

| 3 | Louisiana | 14.33% | 4.40% |

| 4 | Florida | 7.05% | 3.87% |

| 5 | Montana | 5.33% | 3.71% |

| 6 | Connecticut | 8.00% | 3.38% |

| 7 | New Hampshire | 6.25% | 3.30% |

| 8 | Colorado | 5.02% | 3.29% |

| 9 | Texas | 9.44% | 2.97% |

| 10 | Idaho | 6.12% | 2.83% |

| 11 | North Carolina | 8.57% | 2.70% |

| 12 | Rhode Island | 7.34% | 2.55% |

| 13 | California | 4.81% | 2.53% |

| 14 | Illinois | 6.97% | 2.37% |

| 15 | Oregon | 4.95% | 2.09% |

| 16 | Tennessee | 9.21% | 2.08% |

| 17 | Nevada | 5.81% | 2.07% |

| 18 | Alabama | 10.85% | 2.04% |

| 19 | Alaska | 6.00% | 1.94% |

| 20 | South Carolina | 10.38% | 1.63% |

| 21 | Massachusetts | 6.06% | 1.52% |

| 22 | Kentucky | 9.82% | 1.47% |

| 23 | Arizona | 6.72% | 1.24% |

| 24 | Wisconsin | 5.15% | 0.92% |

| 25 | New Mexico | 10.13% | 0.68% |

| 26 | Washington | 4.90% | 0.62% |

| 27 | Pennsylvania | 8.15% | 0.54% |

| 28 | North Dakota | 4.44% | 0.30% |

| 29 | New Jersey | 7.07% | 0.09% |

| 30 | South Dakota | 7.55% | 0.03% |

| 31 | Michigan | 7.76% | 0.01% |

| 32 | New York | 6.50% | -0.13% |

| 33 | West Virginia | 10.63% | -0.19% |

| 34 | Georgia | 8.14% | -0.41% |

| 35 | Kansas | 7.07% | -0.42% |

| 36 | Minnesota | 6.84% | -0.63% |

| 37 | Oklahoma | 8.31% | -0.66% |

| 38 | Arkansas | 11.28% | -1.34% |

| 39 | Ohio | 6.06% | -1.40% |

| 40 | Iowa | 4.15% | -1.58% |

| 41 | Hawaii | 5.36% | -1.83% |

| 42 | Utah | 5.65% | -2.11% |

| 43 | Virginia | 7.05% | -2.21% |

| 44 | Maryland | 7.79% | -2.53% |

| 45 | Indiana | 8.51% | -3.22% |

| 46 | Missouri | 7.17% | -3.34% |

| 47 | Maine | 6.49% | -3.37% |

| 48 | Mississippi | 15.05% | -4.27% |

| 49 | Nebraska | 6.46% | -7.88% |

| 50 | Wyoming | 5.07% | -14.41% |

Note: *No. 1 = Largest Increase

Mortgage payments typically are not reported as late until they are at least 30 days overdue, making it critical for homeowners to catch up on missed payments as quickly as possible.